Q&A: Supplemental Guaranteed Lifetime Income (SGLI)

1. What is SGLI?

A Supplemental Guaranteed Lifetime Income (SGLI) is a separate monthly benefit, also called a supplemental annuity, that an ERS retiree can purchase using funds in Peach State Reserves. SGLI can be used to provide additional financial security during retirement through lifetime monthly benefit payments.

2. Who can purchase a SGLI?

An ERS retiree who is receiving an ERS monthly retirement benefit and has at least $25,000 in the Peach State Reserves 401(k) and/or 457 Plan may choose to use the funds to purchase a Supplemental Guaranteed Lifetime Income (SGLI) monthly benefit by making an irrevocable election with ERS.

Retirees that elected a Partial Lump sum Optional Payment (PLOP) at retirement are not eligible to purchase SGLI. In addition, the retiree must have a minimum of 10 years of creditable service under ERS and make the election before age 70 or the end of the first year of retirement whichever is later.

See number 5 regarding PLOP and 4 regarding the deadline.

3. Why would I want to purchase a SGLI annuity?

Those with a balance in Peach State Reserves will need to manage their PSR funds and withdrawals throughout their retirement. This is especially important for GSEPS members who could have a significant portion of their ERS retirement benefit in the 401(k) plan. SGLI is a way to convert PSR funds into a monthly benefit, guaranteeing you will receive a lifetime monthly income from those funds.

Depending on your circumstances, annuity purchase rates, and financial market performance, a SGLI purchase might be right for you. Various annuity options are available for purchase outside of the ERS plan, through entities like investment and insurance companies, and could be a better option for your situation.

4. When can I purchase a SGLI?

ERS retirees are able to purchase up to two SGLI annuities. All SGLI purchases must be completed before December 31 of the year in which you attain age 70 or, if you first start your ERS retirement after age 70, December 31 of the year in which you start your ERS retirement.

A member may submit a SGLI purchase application with the ERS retirement application. However, the SGLI purchase will not be processed until after the first ERS retirement allowance.

5. Does it matter if I took a PLOP?

Retirees who elected a Partial Lump Sum Option (PLOP) at retirement are not eligible to purchase a SGLI annuity.

6. What funds can be used towards a SGLI?

Only pre-tax, fully vested funds from your Peach State Reserves 401(k) and/or 457 accounts can be used to purchase a SGLI annuity.

See question 8 regarding ROTH funds, 19 for self-directed brokerage accounts, and 20 for rehired retiree information.

7. Is there a minimum amount to purchase a SGLI?

The minimum amount of any purchase is $25,000.

8. Does it matter if my account funds are ROTH?

At this time, funds in a ROTH account cannot be used to purchase a SGLI annuity in ERS.

9. Are optional forms of payment available for SGLI?

Eligible retirees can choose from many of the optional forms of payment available under ERS for their SGLI annuity (with some exceptions including PLOP). The SGLI form of payment does not need to be the same as chosen for your ERS monthly benefit. Please see the 23.6 SGLI Optional Forms of Payment section of the ERS Handbook for additional information.

10. Will post-retirement benefit adjustments increase the SGLI annuity?

No, SGLI annuities are not eligible for post-retirement benefit adjustments that may be granted by the ERS Board of Trustees. If you are interested in receiving increases on your SGLI annuity, you can choose an optional form of pension along with an escalating feature that provides for a benefit that starts out smaller and includes guaranteed increases each year.

11. Is there a SGLI maximum?

The total monthly SGLI annuity amount(s), together with your monthly ERS pension, cannot exceed 90% of your highest monthly earnable compensation while an active member of ERS.

12. How do I apply for a SGLI?

You may request an estimate and application from ERSGA by calling the Call Center. A SGLI application should not be submitted until an estimate has been completed.

13. What if I am concerned about market volatility impacting my PSR funds before the SGLI purchase is completed?

You may use the GABreeze site to access your PSR account and transfer any funds to be used for the SGLI purchase to the Money Market Fund to reduce market risk until the SGLI purchase can be completed.

14. Do I need to designate a beneficiary?

Depending on the option you elect, a SGLI beneficiary(ies) will need to be designated. This beneficiary designation is separate from the beneficiary designated for your ERS benefit and your PSR plan(s).

15. How will the monthly SGLI benefit be paid?

To participate in the SGLI, you must sign up for electronic direct deposit. On the SGLI application form, there is a section to authorize the direct deposit of the SGLI monthly payments along with instructions to provide a voided check which is necessary to set up the direct deposit. Again, this benefit is separate from an ERS retirement benefit and will be paid separately. If there are two SGLIs, there will be a payment for each.

16. When will the monthly SGLI benefit be paid?

Payment will follow the same payment schedule established for the ERS monthly retirement benefit in that payment will be made on the last business day of each month. If you are a new retiree, and both the ERS and the SGLI benefits were requested at the same time, the SGLI benefit will begin one month after the ERS benefit.

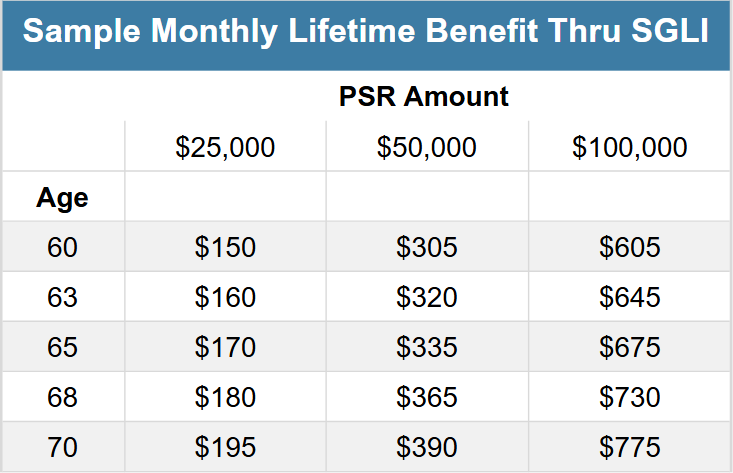

17. How much will I receive under SGLI?

How much you receive under SGLI is dependent upon the amount of funds in your PSR 401(k). An example of your monthly lifetime benefit through SGLI can be found below.

For instance, if you are age 65 and want to use $50,000 to purchase a lifetime annuity, you can receive about $335 each month.

18. Can I cancel my SGLI election?

A SGLI election is irrevocable once the first monthly SGLI benefit is paid. Prior to funds being disbursed from a Peach State Reserves account, an election can be canceled. If you choose to cancel your election after the funds have come out of your Peach State Reserves account & prior to your first benefit payment, only the amount of funds withdrawn would be returned to PSR. You must accept full responsibility for any presumed or real liability or loss from the funds not being invested.

19. How can I get more information about SGLI?

Factors for use in calculating the cost of SGLI annuities will not be available until the end of the 2020 calendar year. Further information concerning the purchase of SGLI annuities will be posted on our website when it is available.

20. Can I use funds in a PSR self-directed brokerage account?

Funds in a PSR self-directed brokerage account (SDBA) may be used, but must be transferred back to your core PSR 401(k) and/or 457 account at least 3 business days prior to submitting a SGLI application. If you are requesting your total balance to be used for the SGLI purchase, then you must liquidate and settle your SDBA, and then process a close out transfer at least 10 business days prior to submitting a SGLI application.

21. What if I am a rehired retiree?

SGLI rollover distributions must follow PSR withdrawal rules. This means that if you are rehired and actively employed by a PSR employer at the time of SGLI application, you will only be eligible for the SGLI purchase if you are age 59.5 for the 401(k) plan and age 70.5 for the 457 plan.

22. Is it better to buy Air Time or SGLI to increase my monthly benefit?

Active members can purchase Air Time at the time of retirement. We recommend active members request an estimate of purchasing Air Time at the time of retirement and for purchasing a SGLI benefit after retirement. Keep in mind that Air Time can be purchased using any eligible funds while only pre-tax fully vested funds from Peach State Reserves 401(k) and / or 457 accounts can be used to purchase SGLI.